GST- Understanding GSTR-1

GST-Understanding GSTR-1

GST filing is one of the most important tasks that every registered business has to undertake. While businesses are supposed to ensure they stay on top of all their filing requirements, GST filing can get a bit confusing due to the many different interlinked forms. Keep reading this article to get an answer to all your doubts regarding GSTR 1.

What is GSTR 1?

GSTR1 is a monthly return or a quarterly return form that every registered dealer is required to file. For most taxpayers, GSTR-1 needs to be filed monthly. In this form, the GST-registered dealers must provide all the details of their outward supplies or sales of Goods and Services.

When is it due?

The due date for GSTR 1 is based on the taxpayer’s Annual turnover. Businesses that have a turnover of a minimum of 5 crores are required to file GSTR-1 monthly and are supposed to file the same on or before the 11th of the upcoming month. However, businesses with a turnover below 5 crores (Amended vide GST Circular No: Circular No. 143/13/2020- GST) can opt for filing GSTR-1 quarterly, and the due date to file it is on or before the 13th of the month succeeding the end of every quarter. For example, the monthly GSTR-1 for the month of March needs to be filed by 11th of April; the quarterly GSTR-1 for the quarter April-June needs to be filed by 13TH July.

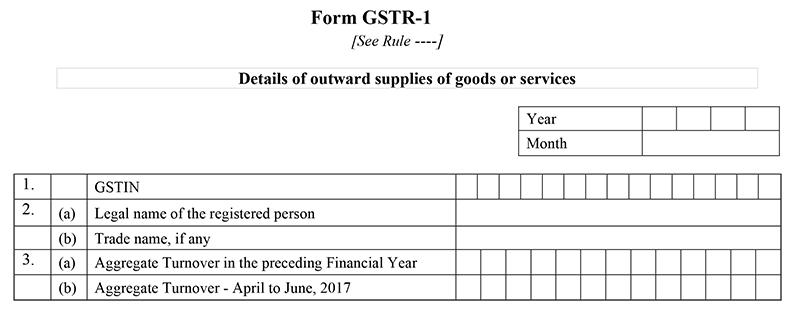

GSTR 1 Form

The GSTR-1 return format in PDF as well as online has 13 sections. Most of these sections are in table format as they require details such as the date of invoice, the rate at which goods were supplied, the different taxes levied, etcetera

- In sections 1-3 of the form, you have to fill in your GSTIN number, your official name, and your gross turnover in the earlier financial year.

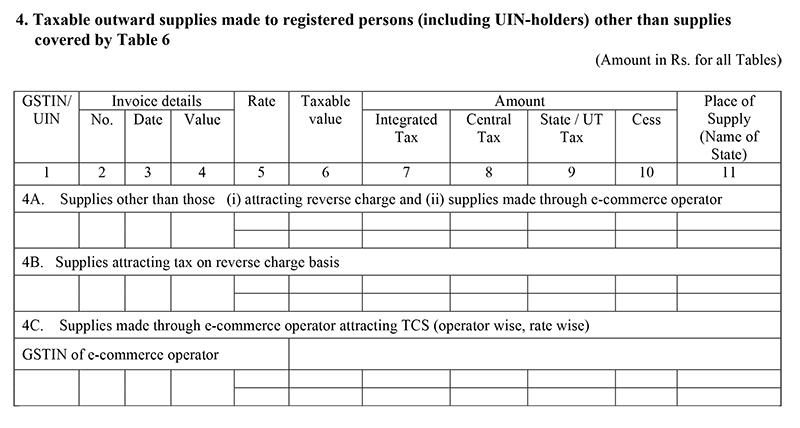

- In section 4, you have to specify the details of all the taxable outward supplies you have made to other GST-registered taxable persons. Outward supplies essentially refer to any products you have supplied or promised to supply.

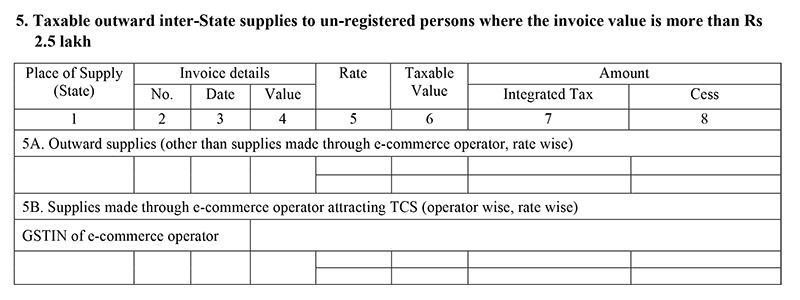

- Section 5 of the form needs you to specify all the details of Interstate outward supplies you have made to GST unregistered persons whose invoice value is higher than 2.5 lakhs.

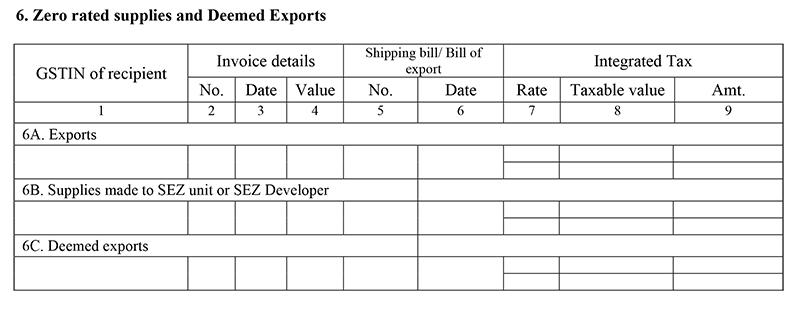

- Under Section 6 of the form, you are to specify the details of zero-rated supplies, i.e., supplies that are tax-free, and the details of exported or deemed exported supplies. Exporters who intend to claim GST refunds on their exports must fill section 6A. Section 6A required one to provide the export data for a specific period. Table 6A of GSTR can be found in the returns section of the GST portal. Every registered taxpayer needs to fill 6B if they want to claim a refund on the taxes they have paid on exports. The exceptions are TCS collectors, compounding taxpayers, input service distributors, and TDS deductors.

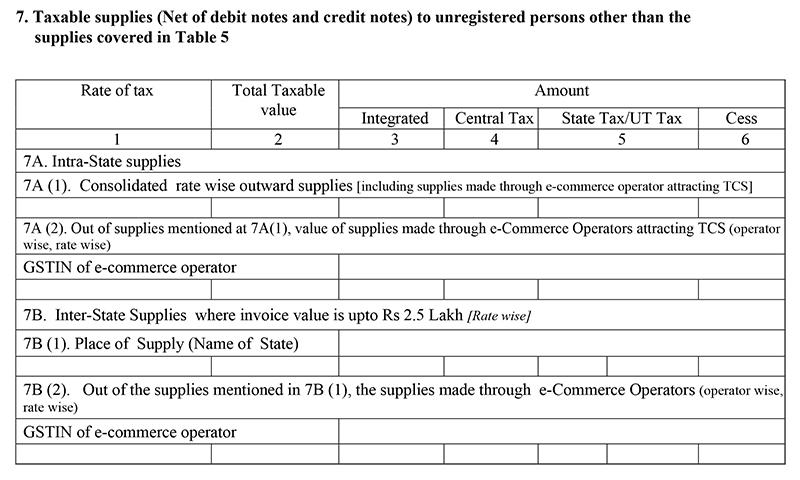

- Under section 7, One has to provide the details of all the items sold to unregistered dealers that have not been covered under section 5.

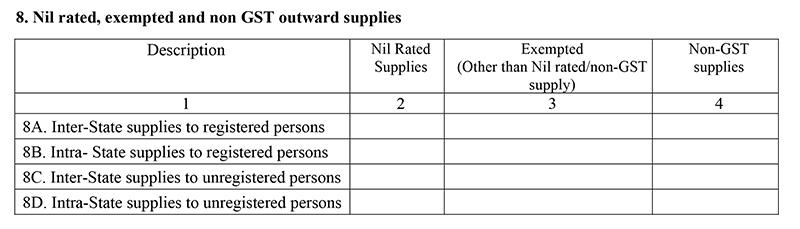

- In Section 8 of the form, you must specify the details of supplies that are non-GST items, NIL-rated, or are items that have not been included in the sections above. These items may have been supplied to registered or unregistered people.

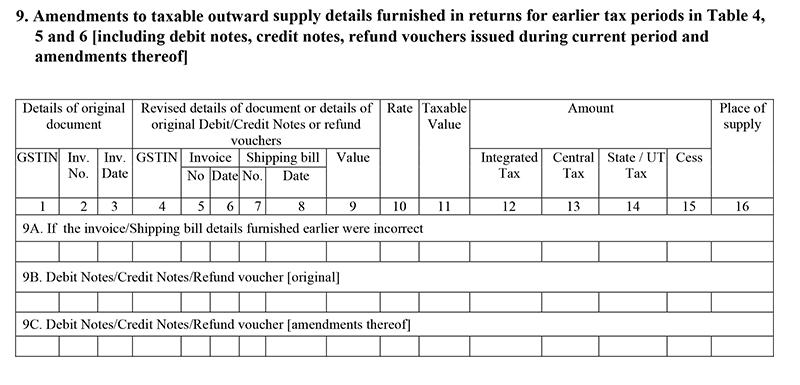

- Section 9 is for making changes or corrections to the information furnished by you in sections 4, 5, and 6. This section is also for you to add any details that you missed out on mentioning in sections 4,5, and 6. You also have to specify the details of debit notes, refund vouchers, and credit notes in this section. If you want to make any changes to the information provided by you regarding the debit notes, credit notes, and refund vouchers, that too has to be specified in this section.

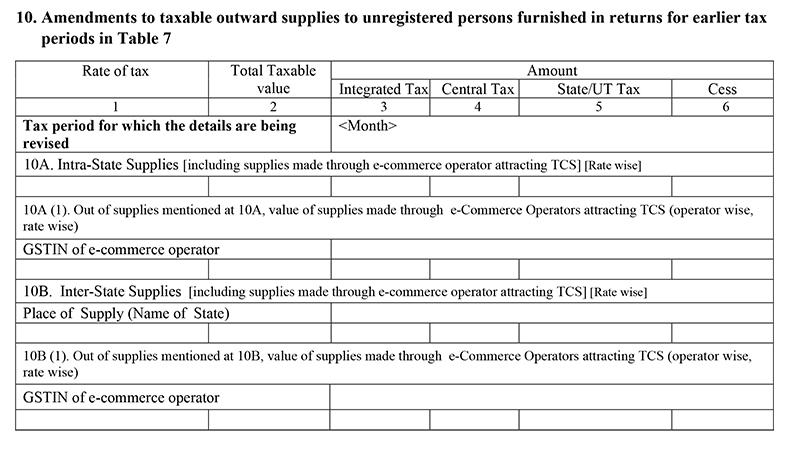

- Section 10 is for you to mention the details of amendments to information furnished by you regarding taxable outward supplies to unregistered persons in an earlier tax period.

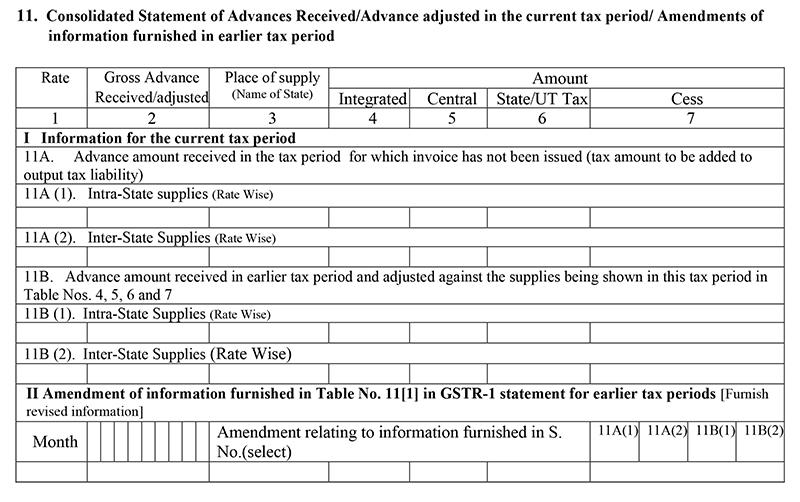

- In section 11, you must provide the details of any advance you may have received and adjusted in the current tax period. If any amendments are to be made to the details you’d furnished in sections 11A and 11B in the previous tax period, that also has to be mentioned here.

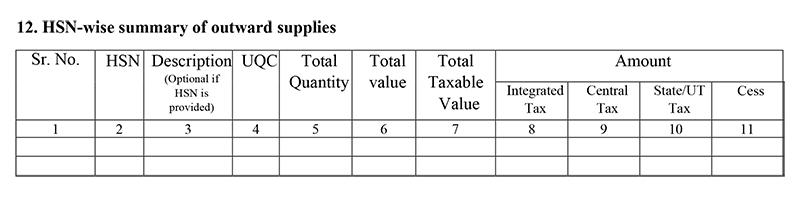

- Section 12 requires you to provide consolidated data of all the taxable supplies via the HSN code. Filling this section is optional for persons whose annual turnover is more than 2.5 crores.

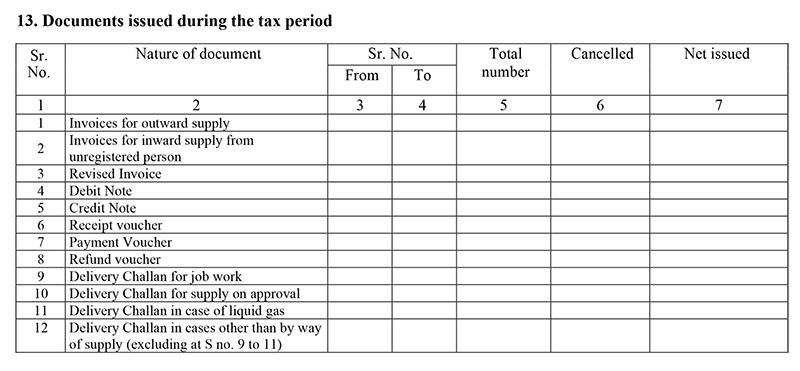

- And lastly, section 13 requires you to provide the details of all the documents issued by you during this tax period, such as invoices, debit notes, credit notes, etc.

Delay in GSTR-1 Filing

Any delay in filing the GSTR-I form or not filing the form at all carries a penalty of Rs.50 per day. Post the 31st GST council meeting, which announced the amalgamation of E-Way bills (EWB) with GSTR-1, taxpayers who do not file GSTR-1 for two consecutive tax periods shall be punished with restricted EWBs.

Examples:

| Date | Duration of delay | Penalty |

| GSTR-1 not filed for the month of March | Ongoing | INR 50 per day until paid |

| GSTR-1 not filed for the months of March and April | Over 2 months and ongoing | INR 50 per day and EWBs restricted |

| GSTR-1 filed 20 days late | 20 days | INR 1000 |

Filing your GST returns can be quite complicated. To get help regarding your GST filing or any quotes regarding GST, just go to LegalWiz.in Our legal experts will guide you through any and all aspects of GST returns, so that you can file accurate returns every time.!

FAQ

- Am I eligible for filing GSTR 1 quarterly?

You are eligible for quarterly GSTR 1 filing if your annual turnover is maximum up to 5crs - Can I file GSTR 1 on the specified due date (11th of succeeding month for monthly and 13th of succeeding month for quarterly)?

Yes, you can file your GSTR 1 on the due date; it is only considered late filing from the next day onwards. - Do I need to file GSTR 1 even if I had no sales this month?

Yes, GSTR 1 need’s to be file irrespective of whether you had any sales or any relevant sales that month. - When can I upload invoices?

You can upload invoices during filing or any time before that as well. We would suggest uploading them earlier or at regular intervals so that you don’t have too much workload regarding uploading invoices on the due date. - Should I file GSTR 1 first or GSTR 3B?

From January 2022 onwards everyone is required to file GSTR-1 before filing GSTR 3B.

Monjima Ghosh

Monjima is a lawyer and a professional content writer at LegalWiz.in. She has a keen interest in Legal technology & Legal design, and believes that content makes the world go round.